Non-deposit products are: not insured by the FDIC;

are not deposits; and may lose value.

Written by: Rodney Hathaway, Chief Investment Officer

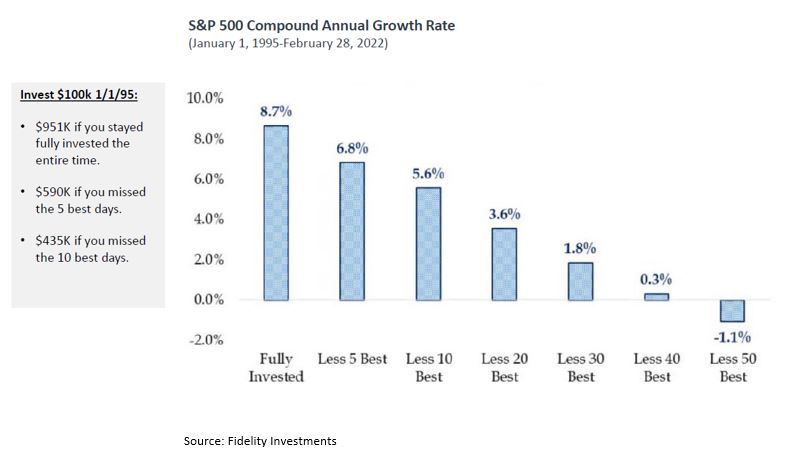

If investors only had a crystal ball to know exactly when the market bottoms so they can jump in or when the market is at the top so they can bail out. This is referred to as market timing. Attempting to time the markets is a common tendency for investors and a practice that many attempt, but very few have been successful. Considering the extent of the sell-off in both the stock and bond markets in 2022, one would expect investors to be extra cautious wading back in to the capital markets. However, if you had sat on the sidelines for the first quarter of 2023, you would have missed a 7% return in the stock market, not a bad bounce back in three months’ time. The large growth stocks that were slammed the hardest last year were up roughly 13% in the first quarter. In fact, if you look at stock market returns as measured by the S&P 500 since 1995, compound annual returns averaged 8.7%. However, had you been out of the market during the five best days during that period, your annual returns would have been nearly two percentage points lower at 6.8%. The chart below just goes to show it pays to be fully invested.

While we may not have a crystal ball, we do have tools at our disposal to limit the risk of overpaying for assets and gauges to help us recognize when prices are below fair value. We refer to these tools as valuation metrics, such as Price to Cash Flow, Enterprise Value/EBITDA or Free Cash Flow Yield. These are basic tools an investor might use to value almost any type of asset, whether they are public securities, private equity, real estate or other hard assets.

The culprit behind the volatility in capital market prices is often attributed to emotional swings of fear and optimism separated by periods of complacency. For example, when interest rates remained low for so many years, most investors assumed that would be the status quo into perpetuity. However, the $6 trillion capital infusion in to the economy in response to the COVID-19 Pandemic created such widespread inflation that the Federal Reserve was forced to take drastic steps to curb wildly rising prices. The Fed’s response of raising short-term interest rates last year was unprecedented in terms of its magnitude of increase in such a short period of time, which significantly impacted stock and bond prices to the downside. Before the pandemic occurred, however, astute investors could have recognized at the end of 2021 many of the popular growth stocks touted on Wall Street were trading at very lofty valuations. Several of these technology-related companies were trading at 10 times revenue. A price-to-sales revenue is a popular valuation metric used by Wall Street analysts when the company is still losing money or has very little net income. When earnings are low or negative, the common price-to-earnings (P/E ratio) method cannot be used since the ratio would be infinitely large or negative. Suffice it to say, paying a 10-times multiple for a company’s revenue is a very rich valuation. As we know, however, when things are good it is difficult to go against the grain and investors are lulled into complacency believing stock prices will go up forever. While the oft quoted S&P 500 was down 18% in 2022, most investors don’t realize that there were several stocks that performed well with solid positive returns. Many of the stocks that were up last year were value stocks in the energy and commodity sectors.

Since it is nearly impossible to effectively time the market, we at Waukesha State Bank Wealth Management believe a prudent approach to investing is to remain fully invested. In an ideal world, you would just make a one-time investment decision and never worry about it again. However, we believe a more effective approach is to remain cognizant of the valuation of the assets in your investment account. Consult with your financial advisor to determine whether the prices you are paying for these assets make sense. As consumers, we generally avoid over-paying for things whether it be a pair of shoes, a meal at a restaurant, a car or a house. Most of us have a good sense of what these items should cost. The same pricing discipline we use as everyday consumers should be applied to your investments as well. As you assess your investment performance over the past few years, you may ask yourself and your advisor whether valuation metrics were utilized effectively in the management of your portfolio. We believe taking an active role in understanding how your investment account is managed is important and can determine whether you reach your financial goals. Work with your advisor to come up with a sound financial plan, review it periodically and make changes as necessary. Most importantly ask questions.

If you’d like help reviewing your situation, Waukesha State Bank Wealth Management is here to help. Please contact us at (262) 522-7400 or wealthmanagement@waukeshabank.com to get started.